In this guest post, Kyle Kroeger from Financial Wolves shares lessons from his journey of paying off $60,000 of student loan debt.

The rise of student loans is a tough pill to swallow—and though repaying these loans is an uphill battle, it’s well worth it.

Students are taking on mortgage-like debt that doesn’t tie to a real physical asset. With student loans, you’re making a bet on yourself to perform well and earn a lot of money, or at least enough to pay off those loans in the future.

Here’s how taking out student loans traditionally works:

- You borrow to get a degree.

- The degree gets you a good job that allows you to make more money.

- Then you repay your student loans over the next 10-20 years. Sound fun?

Not in the slightest—at least, that’s what I thought.

For me, following the mold of putting more money in lenders’ pockets—rather than mine—didn’t sound too appealing.

So I focused on making more money sooner rather than later to repay my student loans. My thinking was: If you focus on your income first, you can repay your debt faster. And once it’s paid off, you’ll cut your expenses, since you’ll no longer have this additional financial obligation.

Below, I highlight three things I learned from repaying $60,000 of student loans.

3 Things I Did to Repay $60,000 of Student Loans

1. I Worked to Be Great, Not Good, at 1-2 Side Hustles

Having a side hustle is excellent; it gives you an extra cash boost that drops straight down to your bottom line of income.

For example, say you get your first job out of college with an annual salary of $60,000.

After budgeting for that salary, add a side hustle to your income. Anything generated from this should be viewed as incremental earnings to your budget, and should only be allocated to repaying student loans or investing at a faster rate.

In other words, this extra income should not be viewed as a way to go on another vacation or buy new pairs of shoes.

For me, I wanted to find a side hustle that I would be great at. Thus, I used my expertise in financial modeling to earn more money. I was able to market my services to small businesses that didn’t have a CFO or finance role. I focused solely on consulting and financial modeling for clients, and worked hard to build a reputation and trust with clients. This led to me building up my hourly rate to $100/hour.

As a result, on any given month, I would make an additional $1,000-$4,000 per month, depending on my workload. Having a valued skill can easily translate into more money for your time.

However, if you focus on too many side hustles, you’ll end up spending more time and possibly earning the same amount of money as you would if you were focused on just one or two that you excel at.

If you have student loans, you likely have a degree. Believe it or not, you learned a lot in college. Apply those skills where they’re needed, and focus on those one or two side hustles rather than spreading yourself thin.

Making money online

As a separate side hustle, I’m a huge fan of making money online by building a website or blog. Though this had a steep learning curve, it was well worth the time to wait and learn because it’s led to new doors in my life that allow me to make money on my own terms.

Blogging can be a great way to learn, earn, and grow no matter where you work. Plus, you can start a website or blog for a very low cost. You already document much of your social life through social media, so why not expand your efforts to blogging to make some additional cash?

I built a few small websites that only cost about $5/month to maintain. I wrote articles about personal finance and generated a small amount of recurring ad revenue. It took me about 3-5 months before I started making meaningful revenue.

Eventually, it turned into $300-$500/month of additional income. This was then used toward my student loans.

Building a small blog made me a better person because:

- It held me accountable in tracking my finances.

- I learned and connected with people around the world.

- I received a lot of constructive criticism from others in the personal finance community to improve.

There are plenty of other ways to make money online, but freelancing and building websites are my favorites.

2. I Developed a Habit of Urgency

In order to pay off your student loans early, you must have a sense of urgency.

Beyond simply having the financial means, people need a mental drive or some kind of motivation. In order to get over the edge, I wrote the following message on a piece of paper:

“Any income you receive above your day job income will go to student loans. Immediately.”

This was a game-changer for me. Every time I got paid, I put more and more toward my student loans.

I was obsessed, and this obsession led to more wisdom along the way:

- If you think that you can’t pay off your student loans early, you never will.

- Small wins go a long way.

- Stay motivated. If you repay $50 of student loans and it doesn’t look like it made a dent, use it as motivation to earn some more money for further repayment.

- Once your student loans are paid off, it’s a gift that keeps on giving. You’ve already budgeted for a life with student loans. Once they’re gone, maintain that lifestyle and you can save at an exponential rate.

3. I Optimized My Interest

How do you know when you should invest versus paying off student loans or credit card debt?

I call it optimizing your interest, and it requires calculating your weighted average cost of debt.

Check out the following table as an example:

| Debt | Debt Amount | Interest Rate | % of Total Debt | Interest x % of Total Debt |

| Student Loan 1 | $10,000 | 6.0% | 40% | 2.4% |

| Student Loan 2 | $15,000 | 4.5% | 60% | 2.7% |

| Total | $25,000 | 100% | 5.1% |

In this example, 5.1% is the weighted average cost of debt.

While getting rid of your student loans is important, investing while repaying is still possible. If you have a very low interest rate on your student loans and your weighted average cost of debt is below what you can earn in the stock market on an after-tax basis, then why not invest?

Done right, you can actually earn more in the long term. However, extinguishing your student loans can go a long way. Thus, I suggest you do a blend of the two.

Consider refinancing your loans

Another way to push down your cost of borrowing and optimize your loans’ interest is, as I learned, refinancing your student loans.

Shortly after college, I found out that I had private loans with a 10% interest rate! I was shocked and knew I had to do something—so I refinanced my student loans all the way down to a 4.125% interest rate. This ultimately saved me over $5,000 in interest payments, as saving money on interest means more money to pay down debt.

When I reached a better interest rate on my loans, I started slowly putting 50% to student loans and 50% to saving for a house. At any given time, I was contributing approximately $500-$1,000 per month toward repaying my student loans.

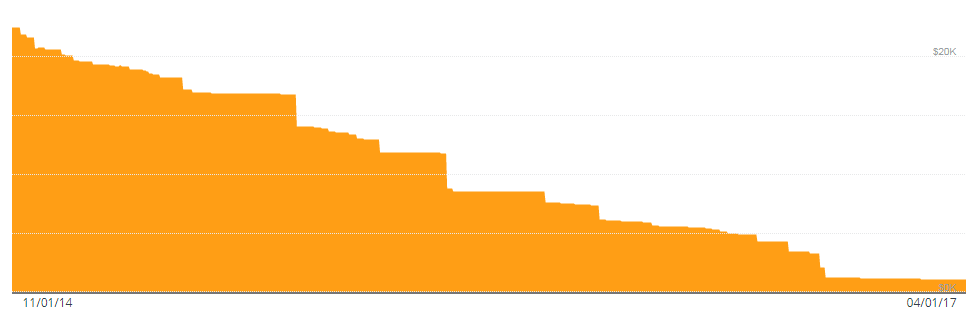

Here’s a snapshot from Personal Capital of one of my few remaining loans over time:

There were even a few instances where I contributed more than $2,000 in a single month toward my debt. Making these large “chunked” payments put a nice dent in my loans, and doing so brought more motivation to the table.

Conclusion

Repaying your student loans might feel like a never-ending journey, but it’s possible to accelerate repayment—it simply requires a strategy for side hustles and full optimization of your payoff plan.

Remember that your student loans are there because someone made an investment in you and your education. Show them that you can outperform their expectations by speeding up repayment. It will put less money in their pocket and more in yours, something everyone should strive for to achieve financial freedom.

Are you ready to repay your student loans? Go contribute an extra $50 to your student loans today to start your journey.

About the Author

Kyle Kroeger is the founder of Financial Wolves, a blog focused on helping readers make more money to achieve financial freedom. After repaying student loans, Kyle has shifted his focus to make more money from side hustles, real estate, freelancing, and the online economy. Follow him on Twitter and Facebook.

Thank you for having my on! Glad I could share my story.